EdTech spend is expected to increase by $2.4 billion in 2021, up from $35.8 billion to $38.2 billion.

2020 spend by America’s K12 schools was captured by the Learning Counsel’s Digital Transition Survey and summarized here.

Technology Spend Increase

U.S. K12 school spend on hardware and major software systems is expected to increase by $400 million or more, going from $22.7 billion to $23.1 billion in annual spend. Many schools still had not been able to obtain the computing devices they needed in 2020 due to shortages, and other schools will be doing some replacements or purchasing for additional grades as needed.

Digital Curriculum Spend is expected to increase by $2 billion, up in 2021 after an already mighty jump in 2020, from $13.1 billion to $15.1 billion. Since so many schools distributed devices in 2020 with very little digital curriculum software investment so far, the majority of digital curriculum companies have reported stellar sales years in 2020 and are also predicting more investment in 2021. A major driver is the need for programs that provide for autonomous learning modes so that all teaching is not via video conferencing. Complaints by parents about “too much Zoom time” have flooded schools since the start of the pandemic and remote learning.

Learning Counsel observations of the overall trends and data include:

Total Revenue

Not all the original CARES Act monies are spent to date. Overall revenues in public sector districts and schools may or may not drop depending on individual state rules regarding funding reductions if there has been a loss of enrollment.

Loss of funds due to student attrition is a major concern for a large number of districts.

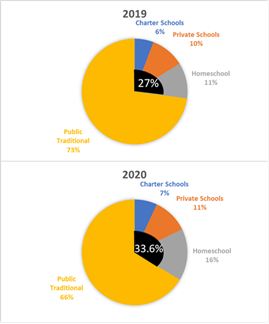

In 2019, Homeschooling Students were the fastest growth segment at 20 percent growth annually. Enrollment loss to homeschooling families has been increasing dramatically for at least ten years but accelerated dramatically during the pandemic.

In 2020, the average defection away from traditional public schools jumped up another 3.6 percent per district. Many districts are experiencing well above that. At this percentage or higher, districts could experience tens of millions of dollars in lost revenue allocation based on state formulas.

The estimate of 33.6 percent of students nationwide now opted out of traditional public schools is conservative. Learning Counsel qualitative review by a sample of districts showed that they have expectations that their current loss of 5-15 percent of all student enrollment will come back after the pandemic and is temporary. Given Learning Counsel’s more comprehensive review of trends towards personalization and a desire by parents for a “consumer experience” in digital learning, there is a high probability that many of these students are gone for good.

While this may affect some school funding, in states like Oregon, the formulas more or less reallocate more funding to fewer students.

Budget Shifts

Learning Counsel analysis of the state of the K12 market includes these potentials to drive the spend increase in technology anticipated in 2021:

- Additional stimulus funds are anticipated from the Federal government.

- Schools are anticipated to cut spend that previously went to paper resources since distributing books or packets during the pandemic is problematic. Major cuts in paper spending were already evident in 2020.

- Schools and districts are anticipated to reduce spend on instructional staffing, primarily through non-replacement of retirees. The largest portion of school budgets are in this area of instructional services, support salaries and benefits at approximately $584 billion annually. Savings in this area have already been fueling increased spend on technology in the last ten years.

- Many administrators will be curtailing capital expenditures for construction where those monies are not encumbered since new building or remodeling investments currently make little sense in most schools. This puts a large part of the approximately $52 billion annually in construction spend in play for technology.

Increased Spend Areas

- Some schools and districts are planning to sunset many of their Chromebooks for upper grades in favor of more powerful laptops so that students can run higher value programs for graphic design, coding, and more.

- Considering Purchase

- 33.5 percent considering eSports software and hardware

- 33 percent considering live tutoring systems/platforms

- 32 percent considering workflow systems (primarily managed document workflow)

- 31 percent considering social-emotional systems

- 29 percent considering standards tracking (and/or scheduling) systems – note these may be defined within modern single sign-on or identity infused education systems

- 28 percent considering dynamic digital inventory systems (for managing the many software subscriptions)

- 26.5 percent considering drones

- 25.5 percent considering digital manipulatives (robotics or other for younger students or science experiments)

- 25 percent considering virtual reality headsets

- 23.2 percent considering coding apps

- 21 percent considering core academic courseware (new purchases), with 67 percent already having some in use (who may be expanding total numbers of license subscriptions)

- 20 percent considering literacy apps (new purchases), with 70 percent already having some in use (who may be expanding total numbers of license subscriptions)

- 16 Percent considering audio enhancement for classrooms (particularly to allow for student’s hearing clearly when more socially distanced)

- 16 percent considering professional grade CTE software (graphic design, video editing, engineering, other)

- 14.5 percent considering supplemental courseware (new purchases), with 74 percent already having some in use (who may be expanding total numbers of license subscriptions)

- 11 percent considering robotics purchases

- 7 percent considering 3D printing purchases

- 5.4 percent considering new purchase of headsets (93 percent citing they have already made purchases of headsets)

- 5 percent considering new purchase of interactive whiteboards or tables (90 percent citing they have some already in use)

Learning Counsel Research completed the 2020 Digital Transition Survey in October. 32,827 educators engaged with the comprehensive survey online. In 2020, there was a 300 percent increase in responses from small and medium schools and districts. 65 schools, districts and service agencies were awarded one of the Learning Counsel’s prestigious EduJedi Levels of Gainer, Innovator, Achiever or Knight.

U.S. Demographics of the survey were:

- 25 percent Urban

- 29 percent Suburban

- 39 percent Rural

- 7 percent Education Service Centers, BOCES, or state entities

Learning Counsel acknowledges and thanks these sponsors for their underwriting of the presentation of the Survey results briefing during the December 2nd Gathering virtual event.

About the Author

LeiLani Cauthen is the CEO and Publisher of The Learning Counsel. She is well versed in the digital content universe, software development, the adoption process, school coverage models, and helping define this century’s real change to teaching and learning. She is an author and media personality with twenty years of research, news media publishing and market leadership in the high tech, education and government industries.